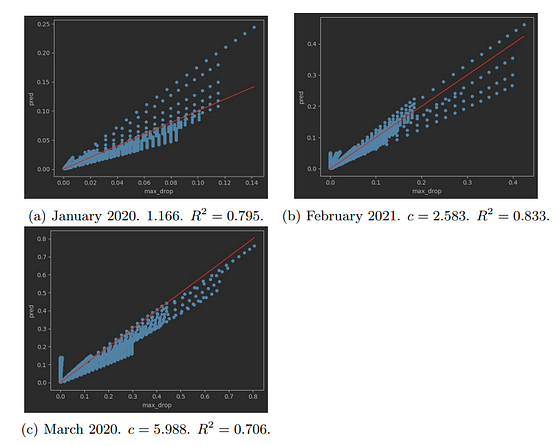

Comparison of simulation results and the results of the formula. For x=0.2, we take all the input parameters for which the simulated max price decrease (max drop) is 0.2, and then plot, in the y axis, the different results and formula give. The red line draws the ideal outcome, i.e., an y=x curve, where the formula returns exactly the same results as the simulation. The R² score is calculated w.r.t the red line.